Europe’s Risky LNG Vision vs. Biden's Political Vision: An Update

US LNG has become an integral part of US foreign policy & national security and they trump climate and environmental policies. However, we must be mindful of the fact that this is an election year!

This is an update to an article we posted on April 10, 2023. We are posting this update after President Biden has put a temporary hold on new LNG export project approvals pending an environmental and economic review, with decisions deferred until after the November 5th election (The impact of politics has been expected long ago, see number 5 below). European and Asian allies, looking to reduce reliance on Russian gas and coal, respectively, watch closely as the U.S., now the leading LNG exporter, faces environmental and industrial pushback. Current projects in question may include those by Sempra Infrastructure and others. Environmental groups, a key segment of Biden’s base, applaud the decision.

Related News:

Reuters: Biden Pauses Approval of New LNG Export Projects

Related Reports:

Global LNG Market in 2023 and Outlook for 2024

EU Gas Imports in 2023 and Outlook for 2024

An Overview of Russia’s 2023 Gas Exports and Forecast for 2024

Trouble in the Red Sea: What’s now for Global LNG Trade?

Nigeria’s LNG Exports Dip amid Growing Local Gas Demand, Output Decline

Canada’s LNG Projects: Prospects and Challenges

EOA’s Quick Take

"As we have been saying: US LNG has become an integral part of US foreign policy and US national security. Foreign policy and national security considerations trump climate and environmental policies. However, we must be mindful of the fact that this is an election year and there is a difference between the short run and the long run. We believe that the Biden administration realizes the role of LNG in foreign policy, but at the same time it needs to show the Democrat base that it is doing something for climate change. Delaying one project or stopping it may not be a big deal, but it is a problem if it becomes a trend. Biden's decision is God's gift to to the Canadian LNG industry"Introduction

Energy security is based on four pillars:

Diversification of energy sources;

Diversification of energy imports;

Low volatility of energy prices; and

Affordability and reliability

Europe has lost all four. European countries are now trying to focus only on solar and wind, while energy imports are dependent on specific suppliers, and prices are extremely volatile. Meanwhile, affordability and reliability have gone out of the window, despite massive subsidies on fossil fuels which several European governments have offered to consumers. Governments, however, cannot continue subsidizing forever and conservation measures have limits. The unintended consequences of such policies can be easily noticed especially when looking at how some countries have recently returned to coal and wood.

The Risks of Depending on US LNG

The US wanted to halt the construction of Nord Stream 2, which was supposed to transport Russian gas to Germany, long before Moscow’s invasion of Ukraine. In fact, in early 2021, 14 months before the war, the US Congress authorized the White House to impose sanctions against companies involved in the project. Even former US President Donald Trump lashed out against the pipeline throughout the second half of 2018. Trump was the “LNG marketing in chief” when he tried tirelessly to convince European leaders to import US LNG instead of Russian gas.

Although President Joe Biden and Trump are on opposite sides of the political spectrum, they are both in full agreement when it comes to Nord Stream 2 and the role of US LNG in Europe. Trump’s success in marketing US LNG was limited, but the Russian invasion of Ukraine created a lifetime opportunity not only to market US LNG but to reserve a market share in the European market for decades to come. As a result, the US has become the largest exporter of gas to Europe instead of Russia in a very short period.

The success of the US in replacing Russian gas in Europe would not have happened without the US shale revolution. We call it a revolution because it flipped the conventional wisdom on its head and changed the direction of trade. Replacing Russian gas in Europe in a very short period has been so radical, enough to label US shale production and exports a “revolution”.

In short, the US LNG industry is the main party benefiting from the energy crisis in Europe. And Europe in its turn has become dependent on US LNG imports. The question of whether this shift was by design or merely the outcome of Russia’s invasion of Ukraine is for historians to answer.

Risks of Increased Dependence on US LNG

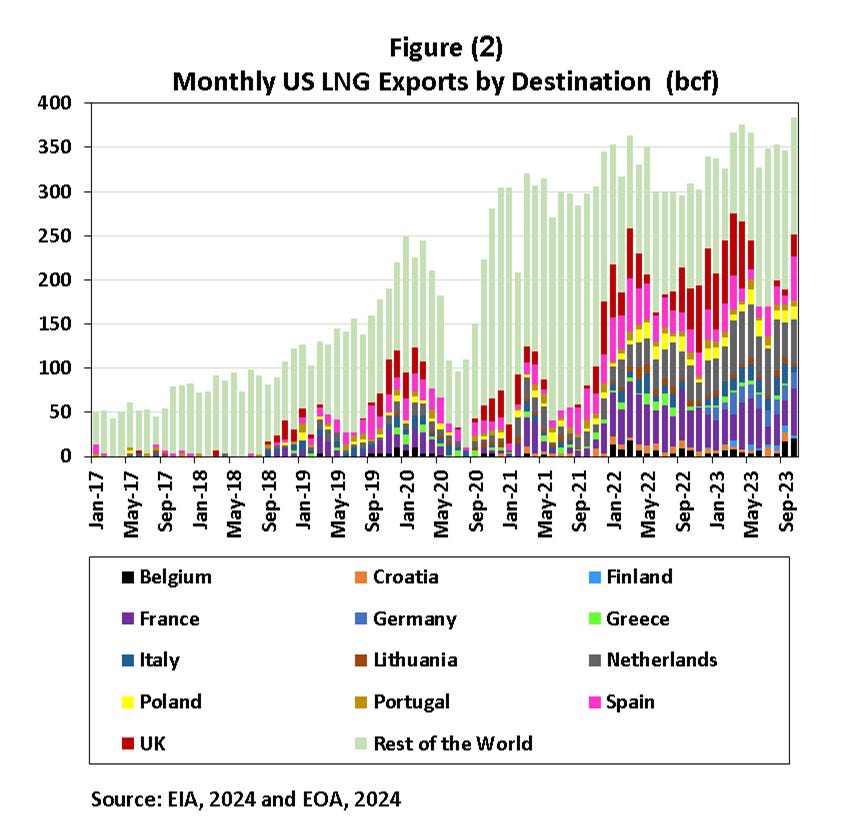

Figure (1) below shows EU gas imports by source in 2023. Piped gas accounted for 53.4% of total gas imports, most of its came form Norway, followed by Algeria. Russia came in in third place.

LNG imports accounted for 46.6% of the EU’s total gas imports, up from 36% in 2022, and 26% in 2021.

In 2023, Norway supplied 29% of the EU’s total gas imports, while Russia (including LNG cargoes) has retained a share of 16.9% of total EU’s gas imports. Dependence on US LNG reached 20.3% of total gas imports. It was about 3%-4% before teh Russian invasion of Ukraine. However, teh dependence of some EU members on LNG imports form teh US is way higher than the average dependence of the EU as a Whole. The top three importers of US LNG France, Netherlands, and Spain as shown in Figure (2) below. However, we have to be mindful of the interconnected gas pipelines and grids within teh EU. For example, what is imported by the Netherlands might end up in Germany via pipelines.

If the EU is concerned about energy security, it will then have to diversify its energy sources and imports as stated above. US LNG, specifically, has certain risks that most other sources of natural gas/LNG do not have. Below are some of these risks:

1- Dependence on Spot Markets

Historically, all LNG contracts have been long-term and linked to oil prices. As the US LNG export capacity developed, a new type of contracts emerged. Meanwhile, there was a change in LNG importers’ behavior toward spot market purchases: as oil prices increased, contracted LNG prices rose, while the market was flooded with spot LNG. As a result, spot prices collapsed. Countries with expiring long-term contracts did not renew, thinking the bonanza in the LNG market will continue. LNG prices increased even before the Russian invasion of Ukraine as competition between Asia and Europe intensified. Prices started to climb to record highs after the invasion.

Europe used to import Russian gas through long-term contracts. Switching from long-term contracts to spot markets implies moving to a very volatile market with a supply risk.

Dependence on US LNG means relying on the spot market for supplies, which goes against the principles of energy security. Europe will face high volatility with excessive prices from time to time as it struggles to compete with China for LNG supplies.

2- Dependence on LNG Instead of Pipelines (Global Competition)

LNG is costlier than piped gas and is more susceptible to interruptions given that tankers in the spot market go to the highest bidder. As Europe embraces additional climate change policies, its dependence on imported and costly LNG cargoes will increase, thus adding extra costs to the energy transition.

In short, Europe was more secure with piped gas because of the existing and dedicated pipelines. Now, with spot LNG and increased global competition, supplies are volatile, and shortages are likely to be seen as LNG demand grows.

3- Dependence on US Hurricane Prone Region

Europe was lucky last winter. The US did not experience LNG disruptions because of hurricanes during the summer when Europe was filling its gas storage. It was also lucky because the winter season was mild.

US LNG plants and export facilities are all located in the Gulf of Mexico. A severe hurricane season in this region means that Europe won’t be able to fill its storage next summer at a time when there isn’t a surplus in other areas around the world. In case this happens, and Europe later faces a severe winter, the continent will be in trouble again.

4- Dependence on Supplies Sensitive to Oil Prices

US LNG supplies can compete in Europe as long as oil prices are high—where the contracted-oil-indexed LNG is more expensive. Should oil prices decline for a few months or more— where the contracted LNG prices decline to below $9 per Million British thermal units (MMbtu)— US LNG supplies will drop. What will Europe do then?

In short, there are problems related to gas price volatility, and others linked to oil price volatility. But here is the catch: should oil prices decline that way, US oil production will fall, leading to lower natural gas production since the tight oil wells produce a lot of gas.

5- Dependence on US Politics

This exactly what happened two days ago when President Biden has put a temporary hold on new LNG export project approvals pending an environmental and economic review, with decisions deferred until after the November 5th election

When US natural gas prices increased, politicians asked the US government to limit US natural gas exports. In fact, the same goes for crude oil and gasoline as US politicians have asked the US administration to limit or even block crude oil and gasoline exports.

Last February, we saw Democrats asking the Biden administration to limit natural gas exports because of the increase in US heating costs. If natural gas exports turn into a national issue, US natural gas supplies to Europe may decline.

6- Dependence on Volatile Shipping Costs

Unlike pipelines, LNG must be transported via tankers, which is a more expensive method. But since LNG is bought in the spot market, the rates of available tankers vary depending on market conditions.

In a tight market, with LNG tankers changing destinations, shipping rates increase. Sanctions on Russian LNG tankers will push rates even higher. This is just another additional volatility element added to the supply and cost of LNG.

7- LNG Maintenance

LNG plants on both sides, the US and Europe require longer downtime for maintenance than pipelines. For now, such maintenance would mean a lower supply. It will take Europe time to build additional gas storage to compensate for a decline in supplies due to this time difference.

8- Cyber Attacks

Anything nowadays is vulnerable to cyber-attacks, and Russian hackers are searching for any weak links. For this reason, a large number of LNG facilities and tankers in multiple countries could be at risk. This situation also means that LNG supplies to Europe could be disrupted at any time.

US Dependence on Europe’s Gas Market

While it is true that Europe is the natural market for US LNG, the growing dependence of the US LNG industry on Europe is likely to generate more risks for the industry (see Figure 2 above). While mild winters and slow economic growth are among the top risks, climate change policies constitute the most significant risk.

Given the heavy marketing of US LNG by the former US administration and the current one, it remains to be seen if European climate change policies will lead to a conflict over US LNG flows to European energy markets. We suspect that there will be a time when the US government will call for a “diversity of energy supplies” to protect the US LNG market share in Europe. (Now we know that the US decided, for domestic political reasons, to stop approval until after the elections).

Going back to Europe, the continent has not fully learned the lessons from its current energy crisis. All that it has done so far is shift dependence from Russia to Norway, and the US, thus making the energy crisis permanent.

Renewable energy cannot replace natural gas in Europe. Other alternatives to US LNG imports have been derailed one after the other: East Mediterranean pipeline, the Nigerian pipeline, and now, because of problems in the Red Sea, future imports from Qatar (Also, that applies to hydrogen and ammonia). If the EU doesn’t want to increase its dependence on Russian gas in the future while focusing on climate goals, it has to build large number of nuclear power plants. Until then, it has to drill for oil and gas in the North Sea and othe rhydrocarbon areas. EOA