China’s LNG Demand Recovery: Drivers and Implications

Last year, China’s gas demand growth was affected by weak demand in the industrial sector due to COVID-related control measures, and high spot LNG prices that were triggered by an unprecedented European appetite for the super-chilled fuel. As a result, China’s LNG imports dropped significantly by 20% year-on-year in 2022 to 63.44 million tons and were surpassed by Japan which has become the top LNG importer. Back in 2021, China overtook Japan as the world’s top LNG importer after reaching all-time high imports of 79.3 million tons, representing 21.2% of the global LNG trade as shown in Figure (1).

Figure (1)

Japan and China’s Annual LNG Imports (mt)

Source: GIIGNL 2022 and EOA 2023

2023 Could See Recovery in China’s LNG Demand

China is set to import higher LNG in 2023 compared to last year due to several reasons. First, a dozen of new LNG term contracts will come into force and kick-start LNG deliveries to the newly commissioned LNG terminals. Six new LNG terminals are ready and need LNG suppliers to begin commercial operations. This could push LNG deliveries to China upward in the next few months.

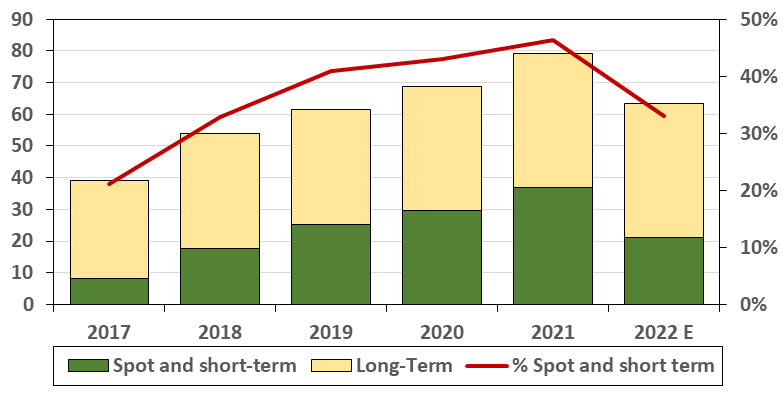

Second, the expected economic recovery following the end of lockdowns could drive industrial and power demand higher. According to the IEA, domestic LNG demand in China could grow by 10% in 2023. Nevertheless, PetroChina, the country’s top gas importer, remains cautious with the IEA’s predictions. Lastly, the price levels of the spot LNG market could incentivize Chinese LNG buyers to obtain more spot purchases. Together with short-term purchases, they meet over 40% of China’s LNG demand while the remaining demand is met by long-term purchases (Figure 2).

This winter, Chinese buyers largely ceased spot purchases in response to weak demand and higher spot prices. Furthermore, the potential increase in spot LNG purchases by Chinese buyers could intensify competition with European buyers when they start filling their gas stockpiles in preparation for the next heating season. Consequently, this could push up spot prices, considering the limited additional global supplies that are planned to come from new projects in the US and Africa.

Figure (2)

China Spot, Short-and Long-Term LNG Purchases (mt)

Source: EOA 2023 and GIIGNL 2022. *2022 data are estimates

Despite the drivers behind China’s potential LNG demand growth, the expected increase in domestic gas production and additional Russian gas supplies through the Power of Siberia pipeline could also limit LNG imports.

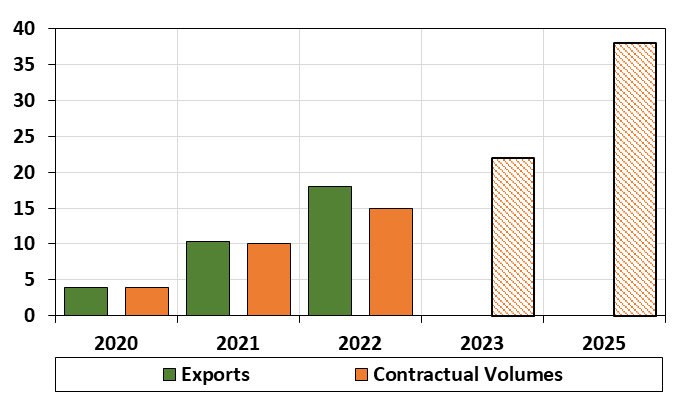

Last December, the Power of Siberia natural gas pipeline became fully operational after the Kovykta gas condensate field in Irkutsk Oblast was put into commercial operations, and the Kovykta-Chayanda section of the Power of Siberia pipeline came on stream. With the newly started section, Russia can ship over 60 million cubic meters of gas per day to China.

In 2022, gas supplies regularly exceeded daily contracted amounts in response to China’s request, Gazprom data shows. The EOA estimates that Gazprom shipped 18 billion cubic meters (bcm) of gas in 2022 through the Power of Siberia to China, up from 10.39 bcm already delivered in 2021. Gazprom is scheduled to increase its exports to 22 bcm in 2023 but the pipeline is not expected to reach its design capacity of 38 bcm per year until 2025 as shown in Figure (3).

Figure (3)

Gazprom Gas Exports to China through Power of Siberia Natural gas Pipeline (bcm)

Source: EOA 2023

LNG Imports in the First Two Months of 2023

According to the EOA’s data, China’s LNG imports dropped 15% year-on-year in January to about 6.24 million tons. In February, however, LNG imports reached 4.85 million tons, an uptick of 1.9% year-on-year (Figure 4). In a positive response to lower prices that hit the lowest level since July 2021 of $13.5 per Million British Thermal Units (MMBTU), Chinese LNG buyers resumed spot purchases in March with one cargo bought by Beijing Gas, and a further two cargoes bought by China National Offshore Oil Corporation (CNOOC). The average LNG price for April delivery into northeast Asia was $13.50 /MMBTU, down nearly 52% year-to-date, and around 80% from its peak in 2022. These low levels are seen as sufficient to attract more Chinese buyers for more activity in the spot market.

Figure (4)

Monthly LNG Deliveries into China in 2022 and 2023 (mt)

Source: EOA 2023

The potential recovery of Chinese LNG demand will affect the global supply-demand balance since there will be a limited additional LNG supply from new projects in the US and Africa. And as we highlighted, this would intensify competition with European buyers when the gas storage filling season starts next summer before the next heating season.