Can Europe Survive without Russian LNG?

EOA’s Main Takeaways

Despite the European Parliament vote to ban the imports of Russian LNG and calls on Ukraine NOT to renew the gas contract with Russia to send Russian gas through Ukraine to Europe, we believe that the top European LNG importers (France, Spain and Belgium) will not ban Russian LNG. They import significant volumes from Russia that cannot be replaced by imports from other countries. Should these countries decide to ban the imports of LNG without any loopholes, it will not only lead to higher gas prices in Europe, but also to higher dependence on coal and a change in global direction of the LNG trade.

“The icebreaking LNG tanker Christophe de Margerie is part of a convoy now on its way from Sabetta to Jingtang, China. (Sovcomflot via The Independent Barents Observer) via Arctic Today, 2020.

On April 11, the European Parliament voted to pass a “legal option” for its member states to limit the arrival of Russian LNG cargoes. This is not a total EU ban.

The new rules allow individual countries to reduce or ban the imports of Russian LNG on their own. We believe that this adopted legal option is more political posturing than policy:

Individual states can decide to ban Russian gas imports on their own anyway regardless of the vote in the European parliament.

The largest importers of Russian gas have no replacement if they decide to ban the imports of Russian gas.

Given the web of gas pipelines among European countries (countries that chose to ban the purchase of Russian gas directly) would end up purchasing Russian gas through other countries!

The situation will be different in a few years when new LNG liquefaction capacity comes online, especially in Qatar and the US. The whole political landscape could be different by then: The war in Ukraine could be over and Putin would be too old or dead. Our forecast calls for a significant rise in demand for gas in Europe, which makes it hard to ban Russian gas even in future years.

Role of Russian Gas in the EU’s Gas Market

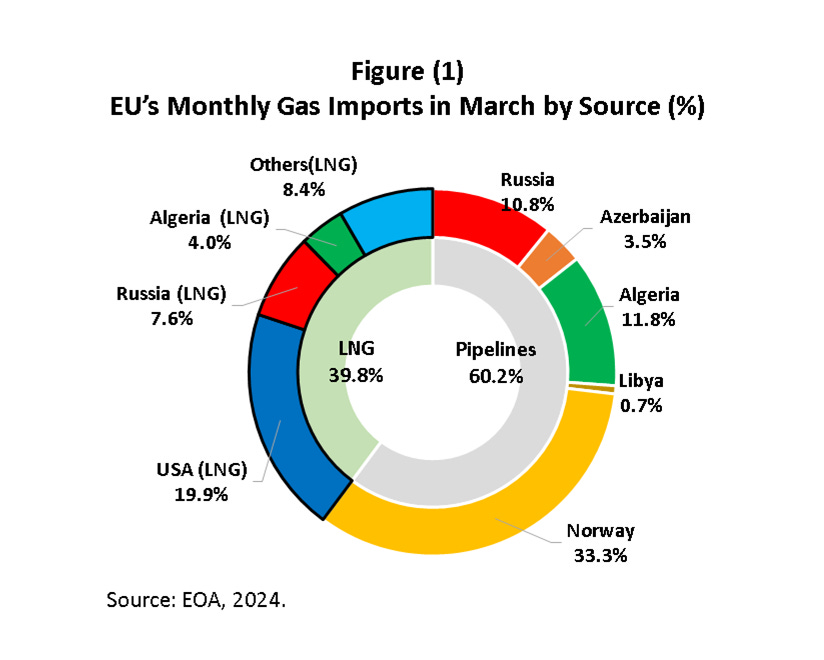

Figure (1) below shows sources of the EU’s natural gas imports last month (March). Gas imported via pipelines accounted for 60.2% of total imports while LNG accounted for the remaining 39.8%. Norway is the top exporter of gas to the EU with 33.3% market share followed by US LNG that accounted for 19.9% of total gas imports. Russia was in third place with a market share of 18.4% (10.8% piped gas, 7.6% LNG). The question is, if the EU bans imports of Russian LNG and Ukraine does not renew the Gazprom contract, where will the EU get the replacement? If it bans only LNG and the Ukraine contract is renewed, there is no replacement for the 7.6%. That could be possible after 2027, but even then, it may not happen if global gas demand is strong.

Figure (2) below shows Russian LNG exports by regional destination. Most of Russia’s LNG exports go to Europe! In theory, a ban by the EU will hurt Russia significantly given the share of exports going to the EU. But a ban will hurt the EU more than Russia.

Who Imports Russian LNG in Europe?

France was the largest importer of Russian LNG in the first quarter of 2024 among EU members, followed by Belgium, then Spain as shown in Figure (3) below. The Netherlands is a small importer. Others are sporadic and small importers and are summed in teh category “other EU.”

The three largest importers, France, Belgium, and Spain, are not expected to ban the imports of Russian LNG, although they might announce plans to reduce or eliminate imports over time. It is important to point out again that while some countries within the EU are not importing LNG directly from Russia, they might end up importing Russian gas via pipeline from countries that import Russian LNG.

Conclusions

Despite the declining role of Russian gas in Europe, its LNG continued to flow into the European market at relatively high levels. Russia was the third largest LNG supplier to the European Union behind the U.S. and Qatar. Although the past two winters were relatively mild, it would have been impossible for the EU to go through them easily with the Russian gas.

The new legal option that was adopted by the European Parliament still needs to be approved by the majority of EU countries before it takes effect. However, even if it passes, its impact is very limited. We believe the largest importers will not ban Russian LNG but they might announce plans to reduce imports or phase them out over a few years.

Although the situation might change by 2027 as more liquefaction capacity comes online, we have to remember that delays are very common in the LNG business. In addition, Egypt is no longer a supplier of LNG. Instead, it is now an importer that is competing with EU members for shipments.

As we stated before, the EU got lucky in the last two years with mild winters in Europe and mild hurricane seasons in the Gulf of Mexico. The probability of having a severe hurricane season in the Gulf of Mexico in the summer followed by a severe winter in Europe is high. Such a scenario would expose the reality of insufficient gas supplies in Europe, even if the winter season starts with full storage. Europe will suffer from shortages and high energy prices, even without a ban on Russian LNG imports and without strong economic growth. The situation in Europe could turn to a crisis if LNG spot prices were significantly higher in Asia and shipments are therefore rerouted to Asia. EOA