Busting Myths about China’s Oil Demand and Imports

Destocking is the next move (With 10 Charts)

EOA’s Main Takeaways

China has replenished its oil inventories. They are near record high.

China will destock as oil prices rise to prevent significant increases in oil prices

The relationship between economic growth and oil demand in China is weakening.

No signs of competition between Saudi Arabia/Gulf States and Russia in the Chinese oil market

We remain bullish on oil, but China will cap oil prices. No $100/b in 2023.

In our EOA 2023 Oil Market Outlook published in January, we told readers that our estimated growth of global oil demand was more conservative than most forecasts due to the struggling economies of China and Europe. We also stated that China’s reopening will have a limited impact on global oil demand in the first half of 2023, leaving the market between a bearish and neutral state. But we pointed out that the situation will turn bullish in the second half of the year. Several analysts believed that the opening of China would be very bullish, but our view has prevailed. In an earlier report, we also argued that OPEC, and during its December 2022 meeting, needed to agree on cutting production in the first half of 2023 to avoid lower prices and an inventory buildup. OPEC, however, did NOT reduce output during that period. By the time OPEC+ members realized last March that they needed to slash production, it was too late. Prices had declined and inventories were already increasing.

The main question is why did most analysts get the China story wrong? Despite several indications, some remained bullish on China, citing strong oil imports. In today’s report, we address this subject to understand on what basis some analysts have built their argument of strong Chinese demand.

Demand vs. Consumption

Before we discuss the difference between demand and consumption, it is important to note that China does not publish data on oil demand. For this reason, analysts use various data points to estimate the “apparent demand’. Therefore, the differences among various estimates are logical and common.

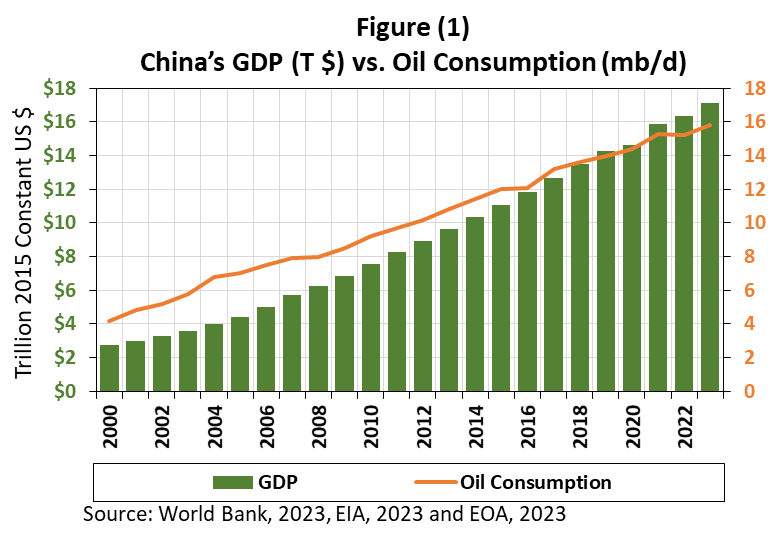

The relationship between oil consumption and GDP growth in developing and emerging economies is well-established in the literature, although it has weakened in recent years due to structural changes in the economy (larger service sector), improved efficiency, and reduced energy intensity. This applies to China as shown in Figure (1) below.

In the oil market, however, the difference between oil demand and oil consumption is storage. With respect to China, the world’s biggest oil importer, some observers fail to distinguish between demand and consumption, and they misinterpret the relationship between economic growth and oil consumption, and that between oil imports and economic growth. Some observers and analysts who got the Chinese growth story wrong drew a link between increased imports and increased consumption, concluding that Chinese economic growth was strong. But once the gap between demand and consumption is factored in, it becomes clear that while China increased oil imports, these cargoes went to storage.

Another issue that was not considered was the difference between oil imports and NET imports. We all know by now that China and India imported Russian crude, refined it, and exported the oil products to Europe and the US, and that’s legal since the G7 and EU-led sanctions allow this process ( what’s not allowed is the transshipment of Russian petroleum products). The bottom line here is that an increase in oil imports doesn’t mean stronger economic growth because some flows end up in storage or are re-exported.

Back to our 2023 Oil Market Outlook, although we got the oil market story right in the first half of 2023, we failed to see the large build in China’s oil inventories. This large build propelled us to adjust our view for the fourth quarter of 2023 and the first half of 2024. While we remain bullish, we are not as bullish as before.

China will release oil from its inventories as oil prices rise, exactly as it did in the past. We learned through the grapevine that Chinese officials have told their Saudi counterparts that they will NOT use their strategic petroleum reserves unless oil prices become too high, such as $100/b or higher. Even if prices hit $100 or climbed above that and China decided to release oil from its inventories as a result, the commercial inventories will be used first, and we need to bear in mind that what is classified as commercial inventories are in reality strategic petroleum reserves. The largest Chinese oil companies are owned and controlled by the central government, while others, like the teapots, follow government orders. In short, China will use its inventories as prices increase, regardless of their classification (strategic or commercial).

In January, we discussed the possibility of oil prices reaching $100 toward the end of 2023. Now, and due to the unforeseen developments mentioned above, we believe that prices will continue to rise, but $100/b is no longer in the picture this year.

The Import-Consumption Myth

Strong oil imports do not mean strong oil consumption, and they don’t imply strong economic growth. Figure (2) below shows the trends in China’s crude oil inventories and imports. Although both sides are not drawn to scale proportionally, our aim here is to show that the gap between the two has been decreasing since the start of the year, indicating lower oil consumption than what some analysts believed. The implications are clear: as we mentioned earlier, we cannot use imports as a sign of consumption. Inventories have increased at a rate higher than that of imports; in fact, they increased to near-record highs.

What Prices Will Force China to Resort to Oil Inventories?

The concept of the SPR in China is different from that in the US. In the US, it is crude oil owned by the federal government, and the US president has the congressional authority to sell and loan from the SPR. The US government, however, has no control over commercial inventories, although there were exceptions. During past wars, Congress enacted laws that granted the government powers over private inventories and to ration domestic consumption.

In China, meanwhile, and although the country has strategic petroleum reserves directly owned by the government, the latter has authority over commercial inventories. Chinese oil majors are owned by the government, while other smaller companies and refineries follow official orders. Claims that China had informed Saudi Arabia that it will use the SPR only if prices increased substantially could be correct because the SPR is owned directly by the government. But what about the inventories that are not directly owned by the government? If we take the Chinese statement at face value, by the time they start using their SPR, they would have already released tens of millions of barrels from inventories that are not directly owned by the government.

The destocking in China may not lower prices, and may not stop the increase either, but by releasing oil from inventories, Beijing will prevent prices from reaching $100/b in 2023.

In 2018, we believed that China would start using its inventories to cap or lower oil prices when Brent prices hit $75/b. We later found out that China had released oil from inventories and lowered imports at $70/b. But what about now? It is hard to calculate a threshold due to the Russian discount. But we believe it is not far from current prices of around $80/b. Once the Russian discount starts narrowing, we believe that the threshold will become lower, between $70 and $75.

Figure (3) below shows the relationship between China’s total inventories (including SPR) and Brent spot prices. The inverse relationship is clear: China has been releasing oil from inventories during high prices and building its inventories when prices drop.

Turning to Figure (4) below, it shows the relationship between inventories and prices. These are two distinct clusters with two distinct periods, and they cannot be analyzed without breaking the data sets. Figure (5) meanwhile shows the two separate parts of this data set. The main takeaway here is that amid lower prices, China builds its inventories, while during higher prices, it withdraws oil from its inventories. These results are significant. Since China’s own crude production has been virtually the same for a long time, the changes in inventories imply changes in imports. Replenishing inventories means higher imports while releasing oil from inventories signals lower imports, and the decline in imports, in its turn, affects global oil prices.

Figure (6) below shows the inverse relationship between China’s oil imports and global oil prices. So far, it is clear from the data that China is actively buying and storing when oil prices are low, and selling when they are high.

Myth of Arab Gulf Competition with Russia in China’s Oil Market

Several media reports have mentioned how OPEC members are losing market shares in the Asian oil market to Russia. We explained in previous reports how the media has been biased in its reporting since West African producers have been the main losers as they were priced out of the Asian market. We also mentioned that the media has ignored the gains of OPEC producers in the European oil market, and the reduced shares of US oil exporters in the Indian market due to strong competition from discounted Russian barrels. In China, which is the focus of today’s report, data clearly shows that there has been NO competition between Saudi Arabia and its Gulf allies on the one hand, and Russia on the other in the Chinese oil market.

We share below three charts to demystify the myth. Figure (7) shows trends in China’s crude oil imports by source, based on Kpler’s data. As imports from Russia increased in recent months, imports from Saudi Arabia remained steady, while flows from the UAE increased. It is also worth noting that the amount of oil imported from unknown sources increased, a sign that the amount of oil imports from Russia and Iran is higher than reported. We are also mindful of transshipments, especially from Malaysia and the UAE. In short, actual imports from Russia, Iran, and probably Venezuela, are higher than what is shown in the chart.

In another development, US crude oil exports to China reached their second highest on record as we highlighted in our Daily Energy Report last week.

To settle the issue of competition between Arab Gulf states and Russia in China’s oil market, we introduce Figure (8). The figure below plots China’s imports from Russia against imports from Arab Gulf states, namely Saudi Arabia, UAE, Qatar, and Oman. We excluded Kuwait because the country cut its exports to China following the start of the Al Zour refinery that was inaugurated at the end of last year. However, Kuwait’s exports to China have remained significant standing at 522,000 barrels per day (b/d) as of June, according to Kpler’s data.

As we explained in previous reports, some media outlets have reported a loss of market share by Saudi Arabia and other OPEC members to Russia by focusing only on percentages. We told readers that if Chinese oil demand is rising, and China is importing the additions from Russia while imports from Saudi Arabia are flat, then percentages, in this case, will show a smaller market share for Saudi Arabia and a larger one for Russia. But from a Saudi point of view, Saudi Arabia did not lose anything since their exports to China have remained flat. But we cannot ignore the Saudi pricing behavior which prevented China from buying more from Saudi Arabia as oil demand increased in the Chinese market.

Figure (9) below covers the data in Figure (8) to percentages. It shows that while the percentage of China’s crude oil imports from Gulf states has been virtually flat, the percentage of Russian imports has risen, and imports of Russian oil through third countries would make this percentage even higher.

So, is China trying to balance its imports to maximize energy security? Or are Arab Gulf producers balancing their acts and avoiding tensions with Russia? Or both?

In our opinion, China is not behaving like India—which has been snapping up Russian barrels at high rates amid lower imports from traditional suppliers like Iraq. Beijing wants to maintain an equilibrium between all oil producers and it is considering relations with suppliers in the medium and long term.

The Use of the SPR

We believe that China will release oil from its inventories, the SPR or commercial oil inventories, to prevent oil prices from rising significantly in 2023. We believe that the current prices and higher ones will trigger a release.

We noted in our first look at 2024 that the most important event in 2024 is going to be the US presidential elections. We also concluded that if oil prices rise in the summer of 2024, the Biden administration will withdraw oil from the SPR, regardless of whether it’s partially refilled or not.

If oil prices rise next summer to the $90s or higher, will the Chinese leadership in this case politicize the inventories, including the SPR? China can influence “gasoline” prices which are crucial for the US election! If this turned out to be the case, China will face a dilemma: they do not want higher oil prices in order to stimulate the Chinese economy, but lower prices will serve US President Joe Biden who is seeking reelection. In other words, if China wants to help Biden, the US president doesn’t have to release oil from the US SPR, because the Chinese will do it for him using their own inventories. But what if China decided not to release any oil from the inventories and keep oil prices high? In such an event, we believe that the Biden administration will release at least 60 million barrels (mb) from the US SPR to lower prices.

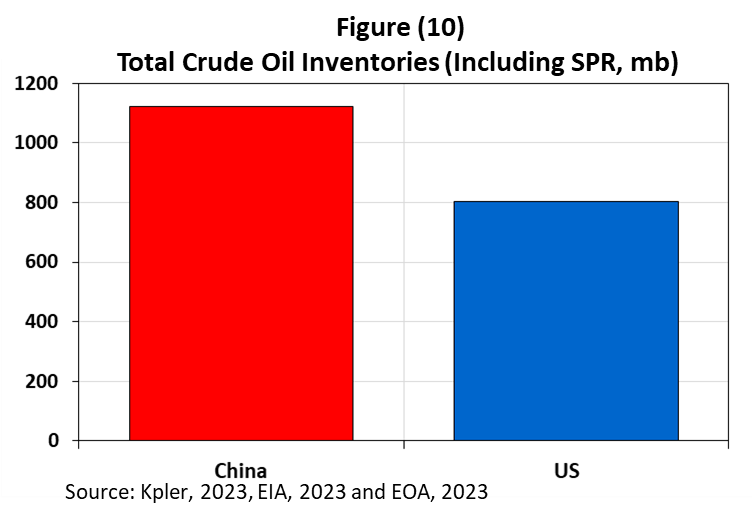

Figure (10) below shows the difference in total inventories. China’s inventories are larger than those of the US, especially if we add about 100+ million barrels stored in underground caverns that are not included in the chart.

Conclusion

As the Russian oil discount narrows and Russia’s crude prices rise, this should lower the incentive of some oil importers, especially in Asia, to import Russian crude and re-export it as refined products. In our opinion, this would be a positive development since it will reduce the current complexity of the market.

China has built its crude oil inventories to more than 1.1 billion barrels. All the evidence presented above points to an inverse relationship between oil prices and imports on the one hand, and oil prices and inventories on the other. As oil prices rise in the next few months, China will release oil from its inventories and lower imports. Such measures will affect oil prices by capping them or limiting their growth. Our view is that if prices continue to increase, China will release about 80 mb from its inventories over the next five months, accompanied by an almost equal reduction in oil imports. However, even under such a scenario, oil prices will rise in 2023, but only by several dollars above current levels. EOA